Quietly furious, Mostly Unaware, and Betting Less... The Freebets.com Betting and Trends Survey 2026

Joshua Kerr

Joshua Kerr  Dominic Celica

Dominic Celica

On 1 April 2026, the UK government doubled the Remote Gaming Duty on winnings from online casino products, including slots welcome offers and welcome bonuses, from 21% to 40%.

The industry is bracing for impact. Punters, by and large, haven't noticed yet but they have noticed the offers shrinking around them.

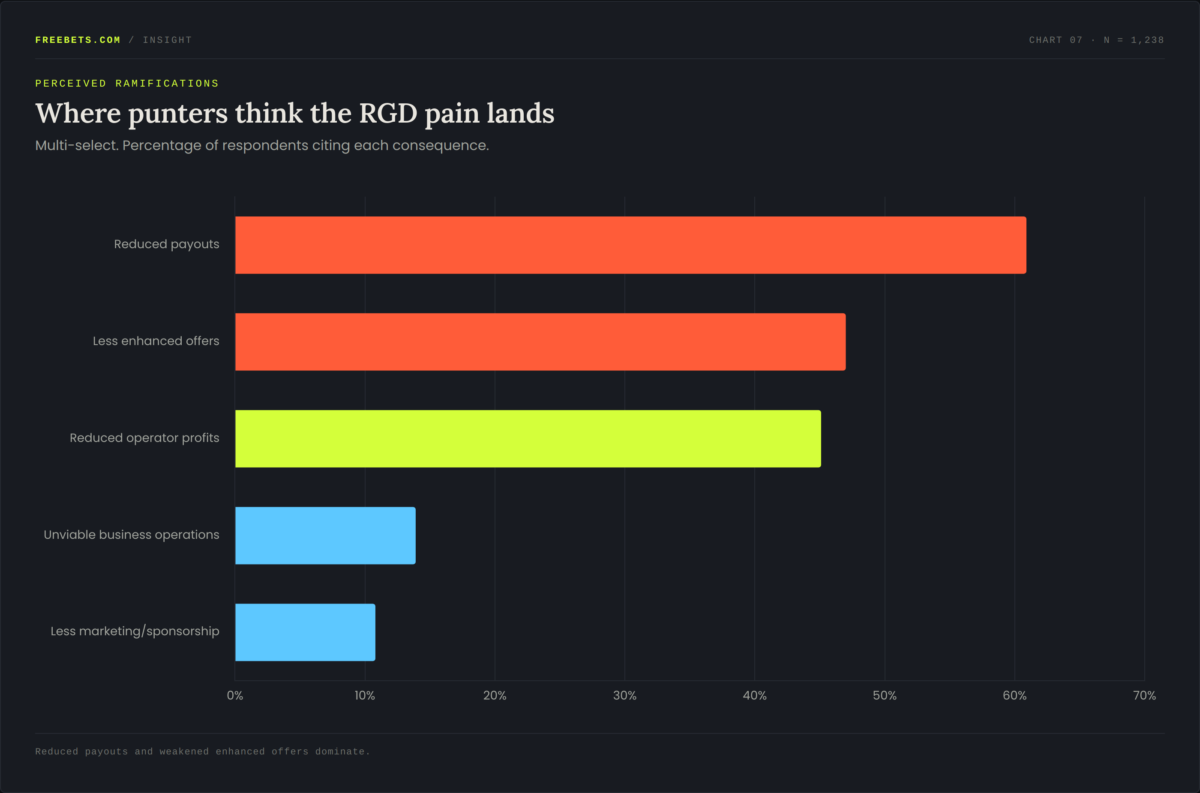

When we asked those who were aware of the change what they believed the biggest ramifications would be for UK licensed betting sites, the most common responses were reduced payouts (61%), fewer enhanced offers (47%) and reduced profits (45%).

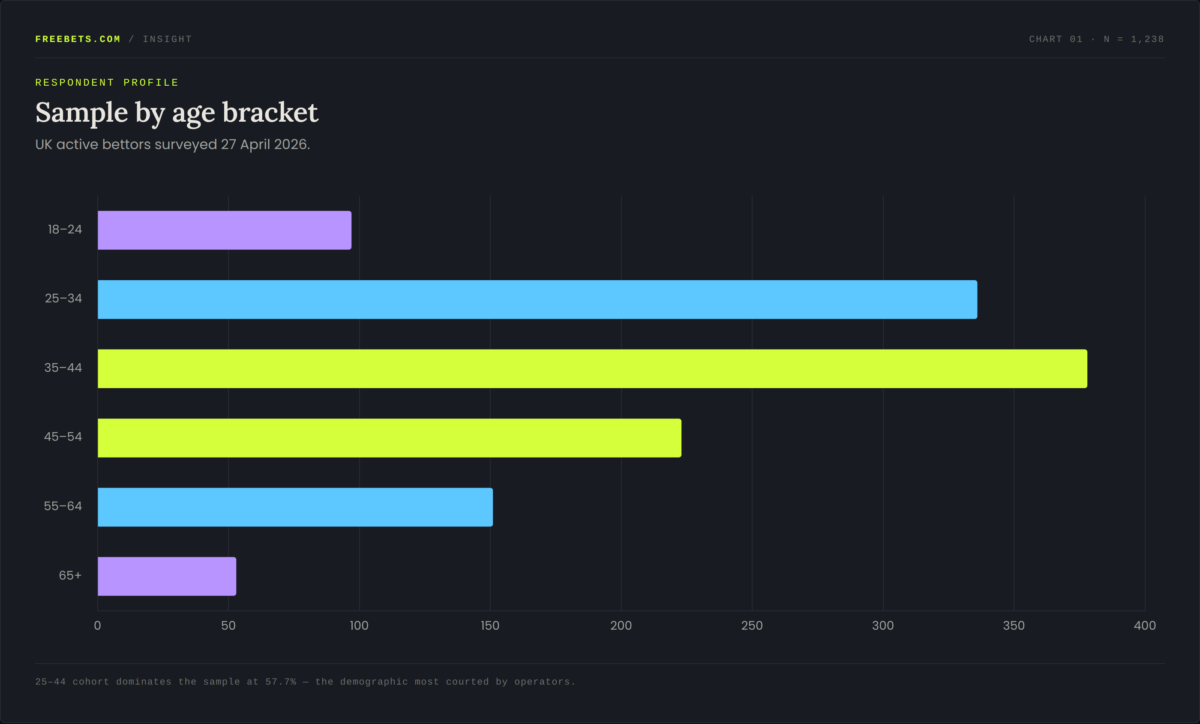

A representative slice of the recreational British punter

The sample skews towards the core working-age bettor, with 57.7% of respondents aged between 25 and 44 - the demographic most courted by both operators and affiliates.

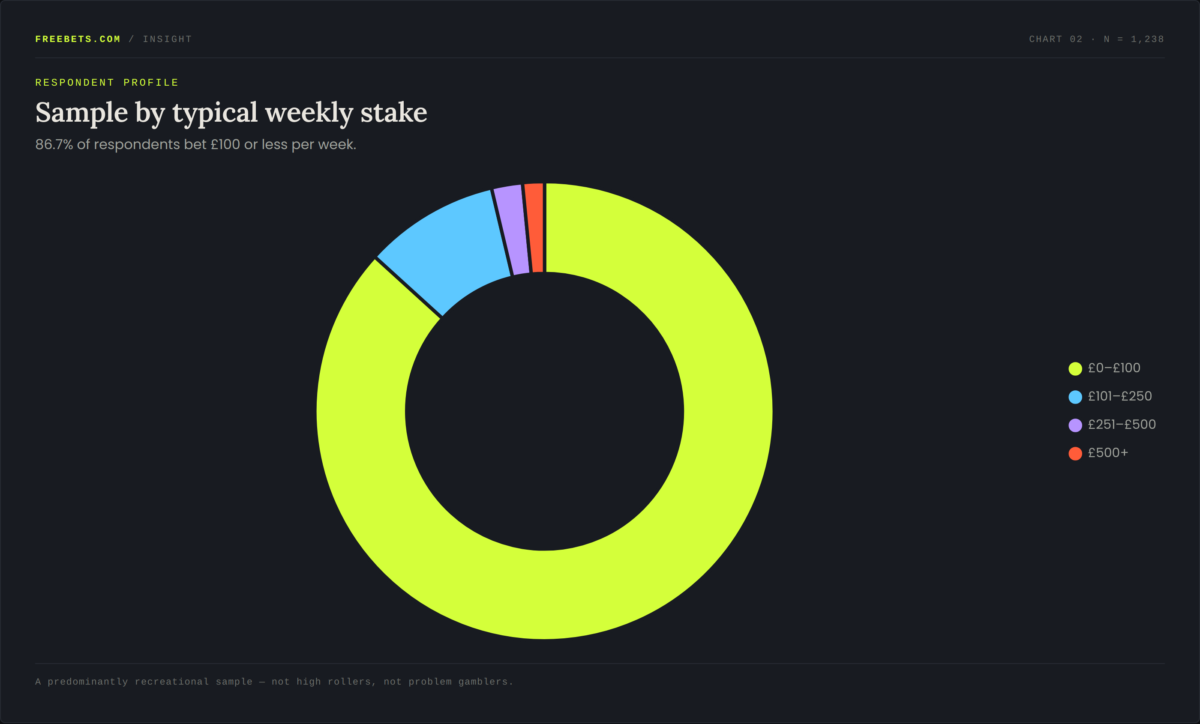

Stake levels confirm this is overwhelmingly a recreational sample: 86.7% bet £100 or less per week. This is the silent majority of the UK gambling market, not high-rollers, not problem gamblers, but the everyday punter for whom margins on offers and odds materially shape behaviour.

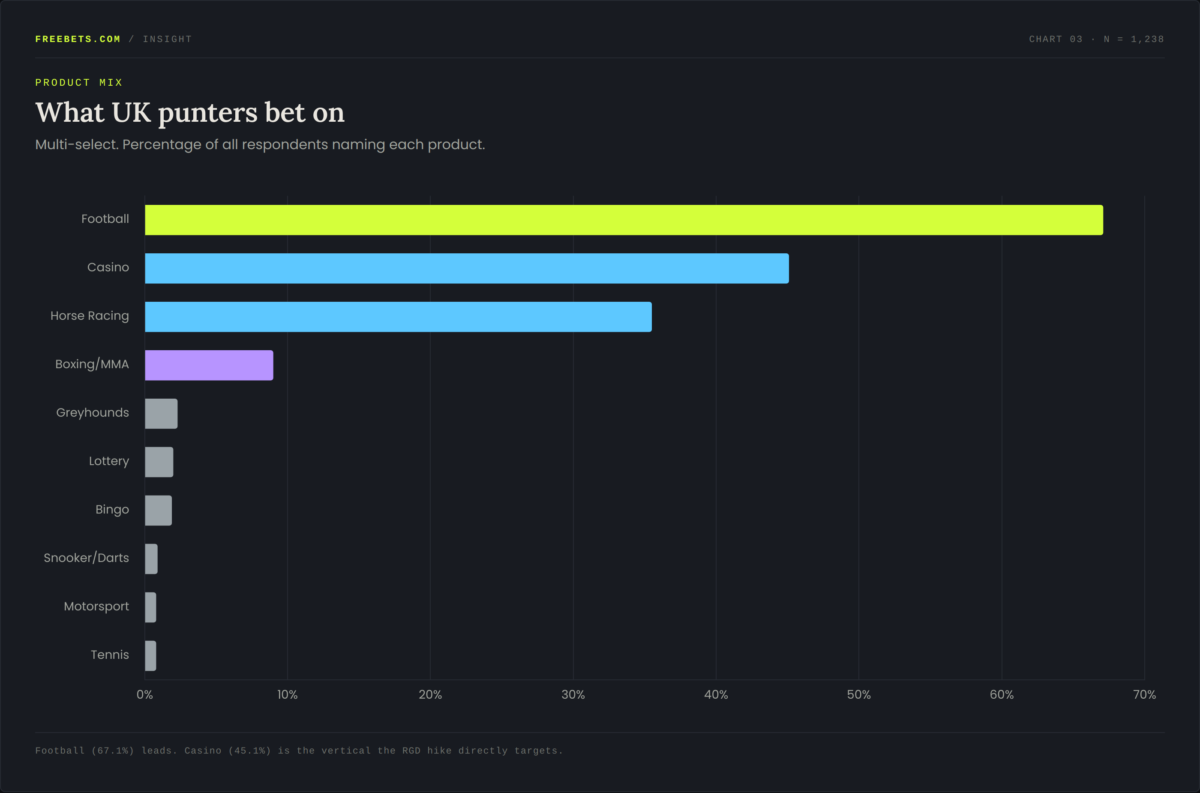

Product mix: football leads, casino lurks

Respondents could select multiple products. Football was named by 67.1% of the sample, comfortably the most popular category, followed by casino at 45.1% and horse racing at 35.5%.

The combination of football and casino is the structural backbone of the modern UK gambling consumer, and crucially, casino welcome bonuses are precisely where the duty hike lands hardest.

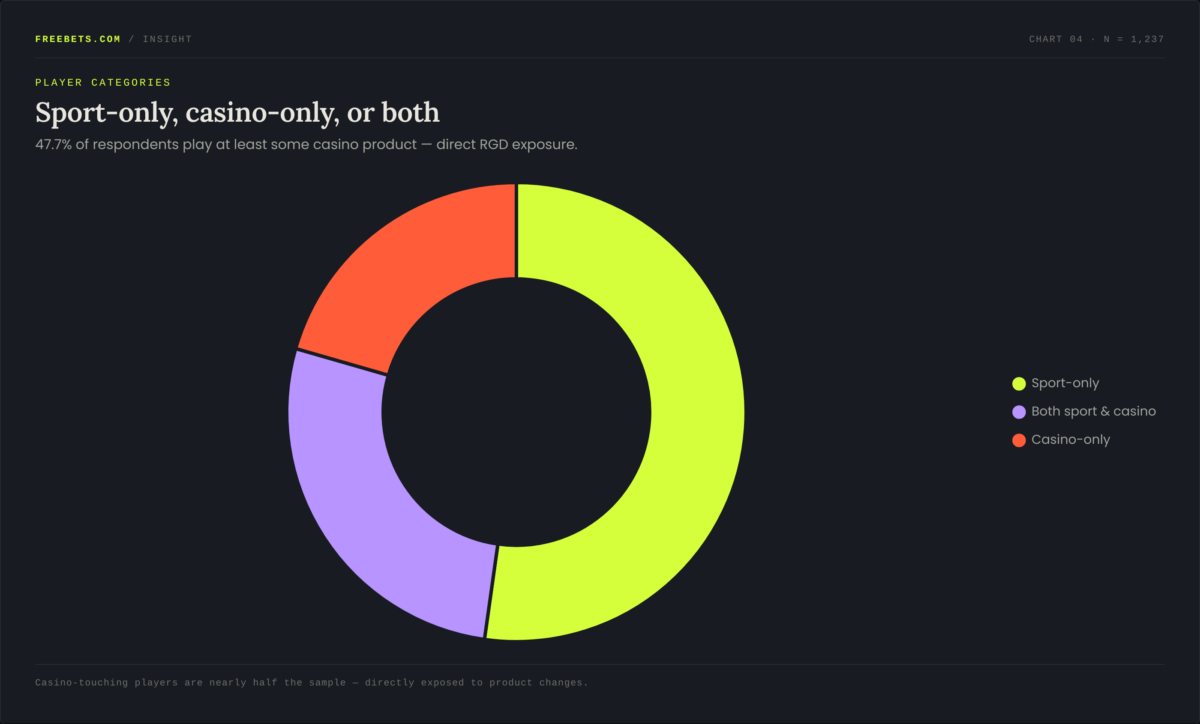

Slicing the sample by what people play: 52.2% are sport-only bettors, 27.2% use both sport and casino products, and 20.5% play casino exclusively.

The casino-touching cohort (close to half the sample) is therefore directly exposed to RGD-driven product changes, even when they remain unaware of the policy. This split becomes critical when we examine future behavioural intent later in the report.

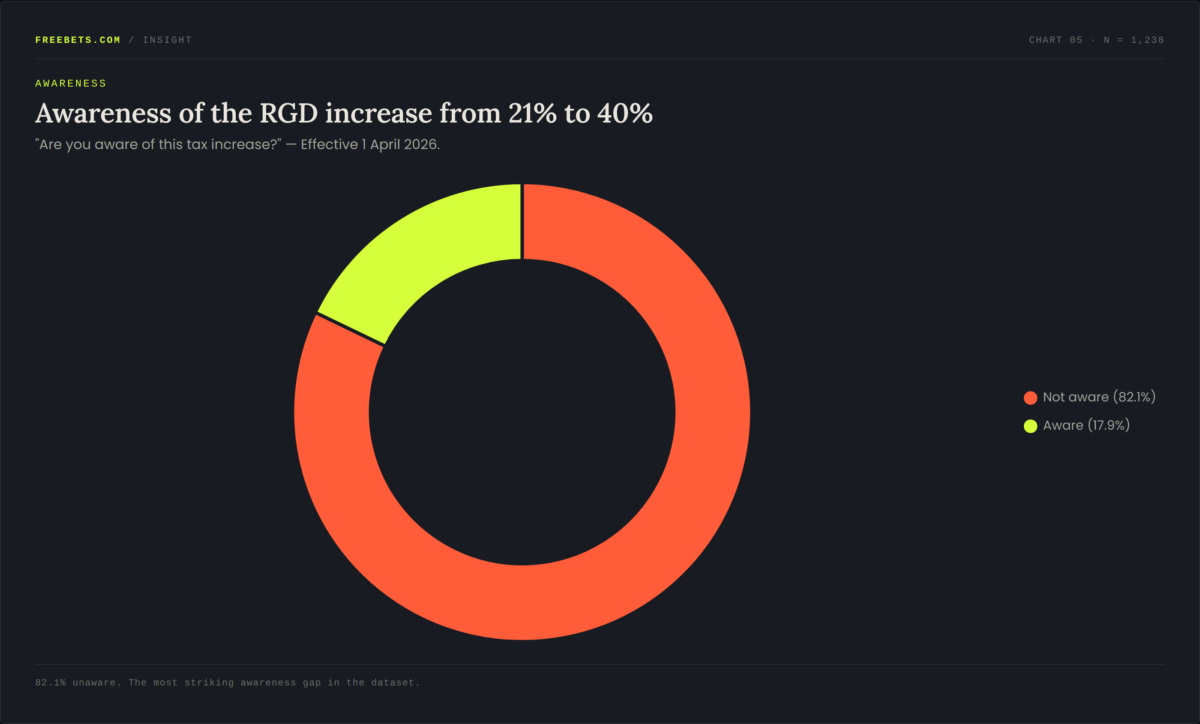

The Awareness Gap: A near-doubling of RGD duty, and almost no one knew

The RGD hike was extensively trailed, publicly debated through the autumn 2025 Budget cycle, dissected at iGB Affiliate London, and front-page material in trade publications. None of that landed with the consumer.

And this is not a niche issue: a 19-percentage-point increase in duty represents one of the most significant fiscal shocks the licensed online gambling market has ever absorbed. And yet the punter, the ostensible end-recipient of the consequences, does not yet possess the vocabulary to discuss it. When they describe what's wrong, they reach for the symptoms: smaller free bets, worse odds, fewer Cheltenham specials. They do not reach for the cause, because 82% of them don't know about it.

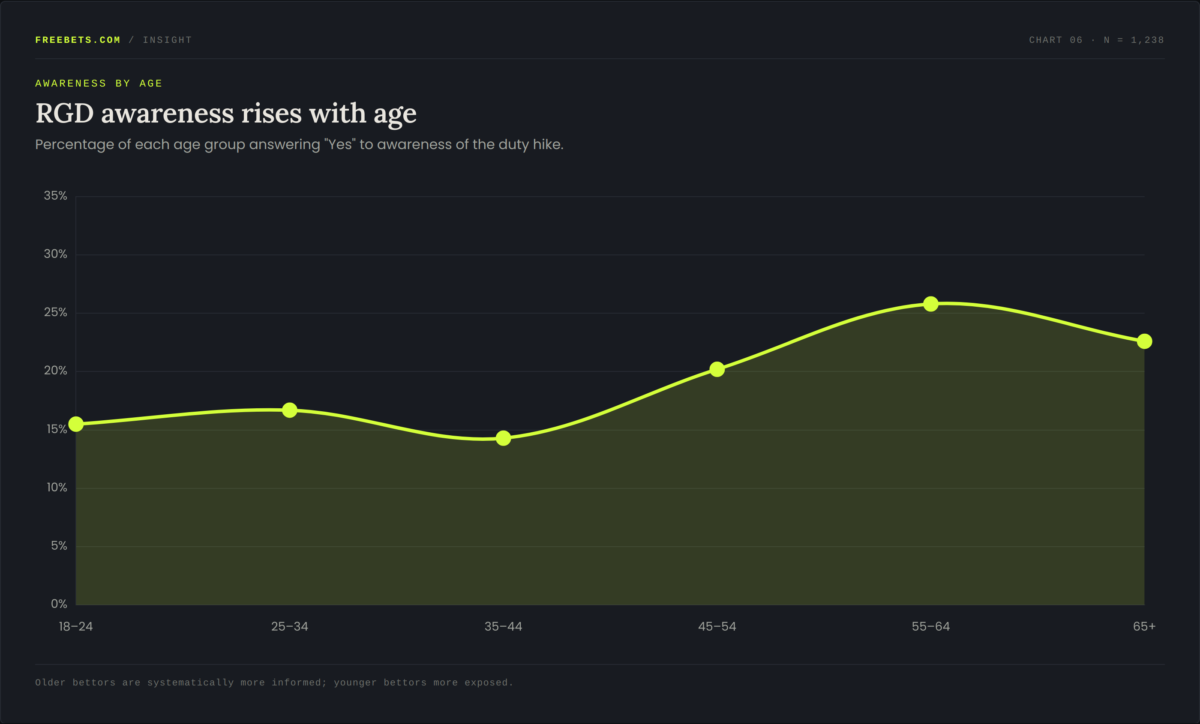

Awareness skews older

One of the more interesting cuts is awareness by age. The under-45 cohorts, exactly the demographics operators target hardest, are least aware of the duty change. Among 25–34s, fully 83.3% had not heard about it. Awareness rises notably with age, peaking at 25.8% among 55–64s, suggesting that the issue has cut through to traditional media consumers (newspapers, broadcast news) more effectively than digital channels.

Implication: Operators bear the entire communications burden in this environment. There is no public consensus that "things are worse because of the tax" meaning every degraded promotion, every narrower price, every withdrawn bonus is read as a brand failing rather than a fiscal one. The industry is taking the hit twice: once at the Treasury, and once in customer goodwill.

Where punters think the pain lands

When asked what they considered the most significant operator-side consequences of the duty hike, respondents pointed first to the customer-facing erosion - payouts and offers - rather than to the structural pressures on operators themselves. The order of concern is telling: punters see the industry through the lens of what they're losing, not what bookmakers are absorbing.

The top three responses, reduced payouts (60.9%), less enhanced offers (47.0%), and reduced operator profits (45.1%), together describe a market in which customer experience and operator economics are seen to be deteriorating in tandem. The implication is that punters do not view this as a zero-sum transfer between bookmaker and bettor; they recognise that everyone is losing, even if the policy mechanism remains opaque to them.

The lower-ranked responses are equally revealing. Only 13.9% cited "unviable business operations" and just 10.8% noted "less marketing and reduced sponsorship". Both are real, ongoing structural consequences in the industry, yet neither is visible to most consumers. This is a gap freebets.com and educated affiliates can usefully fill.

"Bookmakers should not expect the punter to be penalised financially as they make millions in profit 100% of the time. Pass profits on to keep gamblers happy." - Casino player, 55–64, £0–£100/wk

"The government's decision to increase taxation is incredibly shortsighted. 'Problem' gamblers are still going to gamble. If the odds and offers available from regulated bookies and casino operators get worse..."

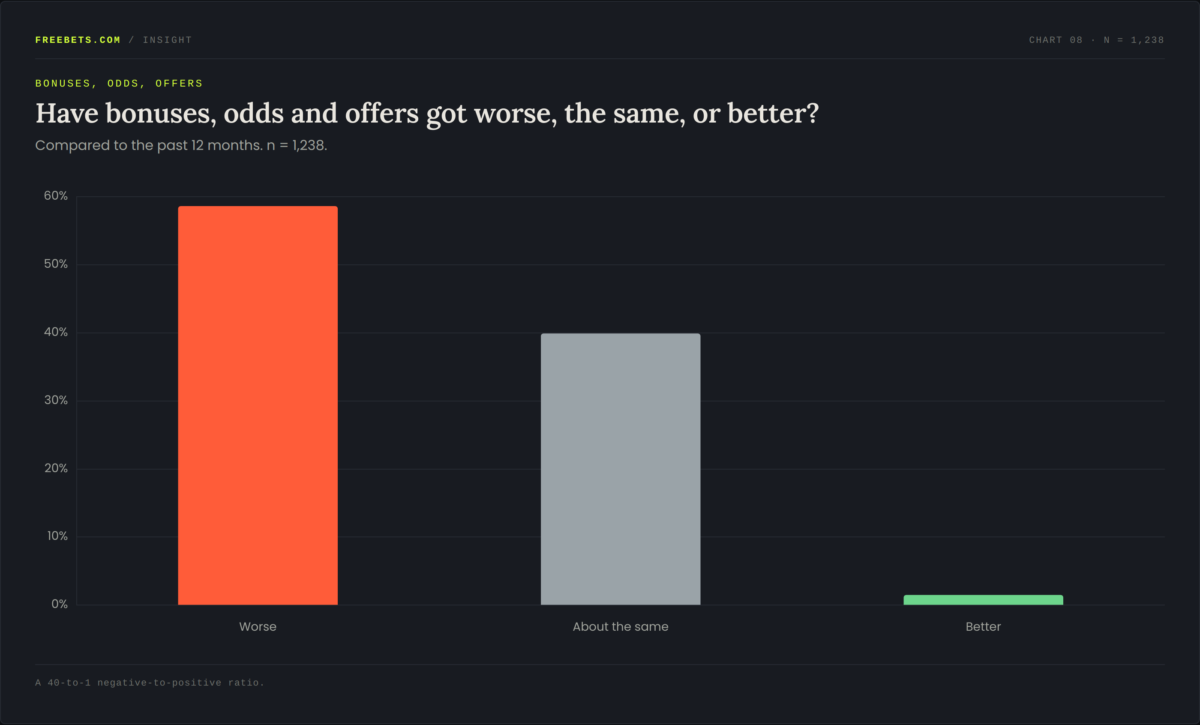

Bonuses, Odds and Offers: The clearest verdict in the dataset: worse

Asked whether their bonuses, offers and odds had got worse, better or stayed the same over the past twelve months, respondents delivered the most one-sided result of the survey. 58.6% said "worse". Just 1.5% said "better". The remaining 39.9% sat at "about the same", but in a market where rising stake values, increased operator marketing investment and improving live-pricing technology should logically produce upward pressure on player value, "the same" itself reads as a soft negative.

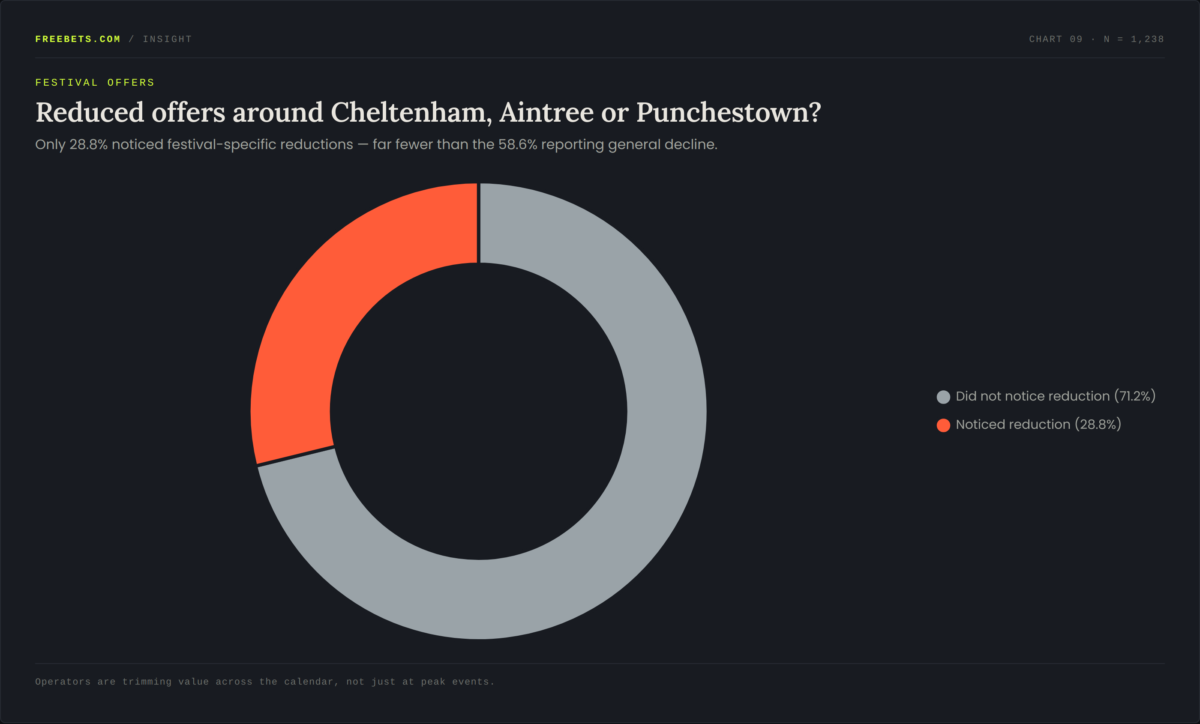

The festival effect: not where you'd expect

One of the most interesting cross-checks in the survey concerns the spring National Hunt festivals. We asked specifically whether respondents noticed reduced enhanced offers and bonuses around Cheltenham, Aintree or Punchestown. Only 28.8% said yes, far fewer than the 58.6% who reported a general decline.

This data matters. It tells us that the perceived offer decline is not festival-specific or product-specific, it's pervasive. Punters experience the contraction in their everyday casino spins, weekend football accumulators and midweek racing markets, not just at peak racing windows.

The implication: operators have generally trimmed value across the calendar rather than absorbing the duty by leaning into known peak-acquisition moments. Bookmakers continue to price their hero events competitively because they know the matched-bettors and arbitrageurs are watching; they pull margin out of the long tail instead.

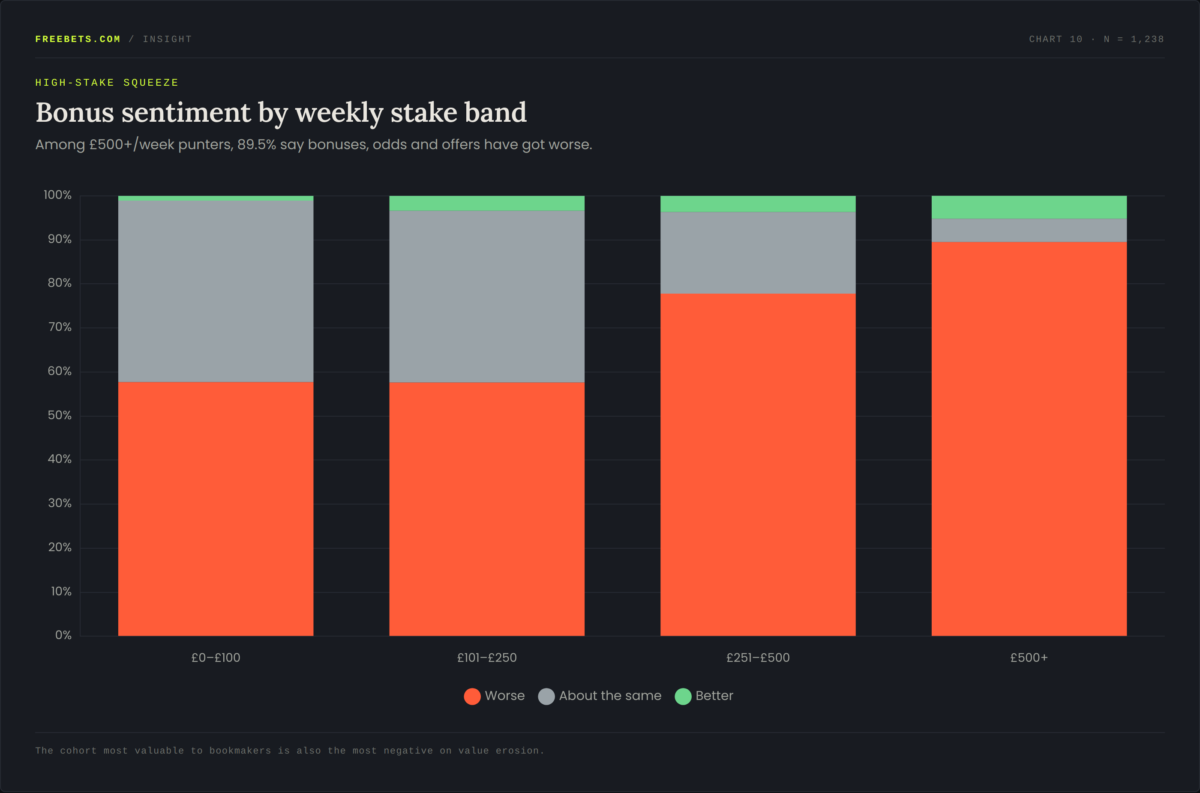

Bonuses sentiment by stake band - the high-roller signal

The most telling cross-cut in this section is bonus sentiment by stake band. The pattern is almost linear: the more you bet, the more strongly you feel value has degraded. Among £0–£100/week recreational bettors, 57.7% report a worsening. Among £251–£500/week bettors that climbs to 77.8%, and among £500+/week punters it reaches 89.5%.

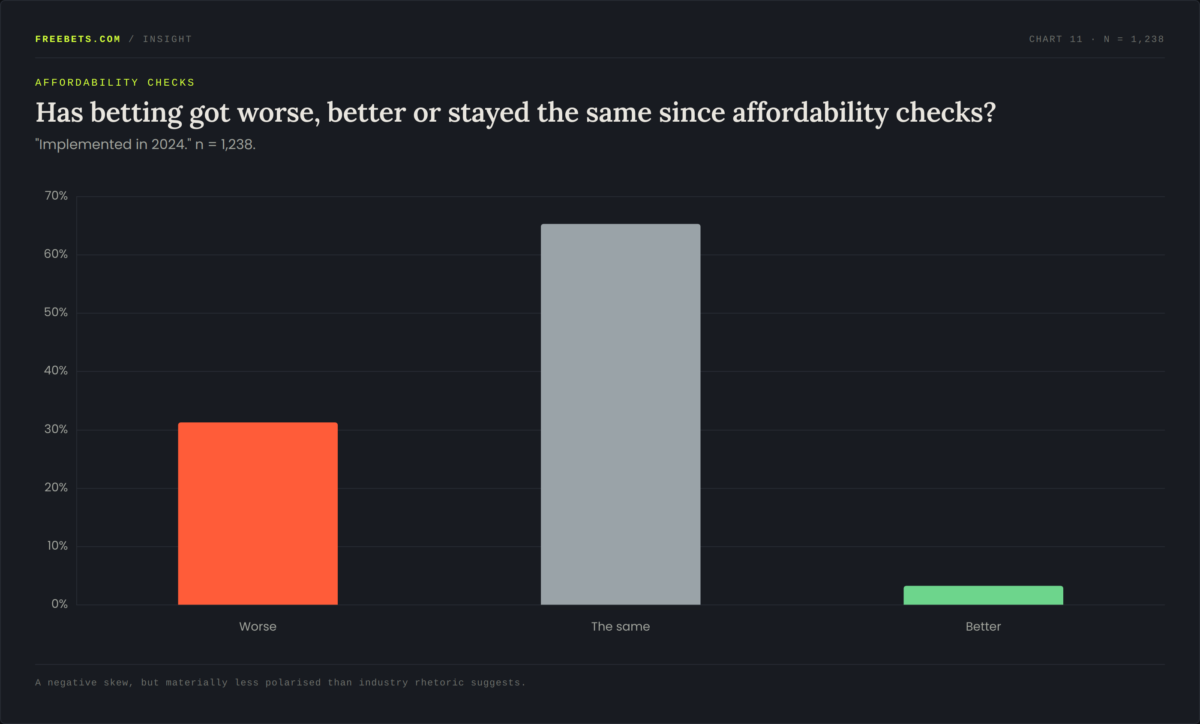

Affordability Checks: Almost a Third Say it's Made Their Betting Worse

Affordability checks generated significant media and political heat since their 2024 introduction, but while the majority - 65.3% report that their experience has stayed "the same" - almost a third (31.3%) describe the new checks as making their betting experience worse. Barely anybody, just 3.3% actively say their experience has improved...

The qualitative responses we received reveal a sharp edge. A meaningful sub-segment of respondents see the checks as an erosion of personal autonomy and a friction point that is contributing to the overall sense of a degrading product. The two issues: 1. duty pressure on offers, and 2. intrusion via affordability combine into a compound dissatisfaction even when each is individually digestible.

"The affordability checks make it feel almost illegal and need to go. It's become a bit nanny state with the way they constantly have to remind you about gambling addiction. It's like a guy in the pub handing over a pint and giving you a lecture on the dangers of alcohol." - Football bettor, 35–44, £0–£100/wk

"I have had two gambling accounts closed because I am not willing to send in identification or wage slips. I believe this stuff is aimed at monitoring people rather than keeping them safe. People have a right to privacy." - Respondent aged 45–54, £0–£100/wk

The recurring theme is one of responsible adults objecting to being treated as suspects. Respondents repeatedly distinguish between sensible safer-gambling tooling, which they support, and intrusive document-based affordability checks they regard as an erosion of consumer privacy. The takeaway for affiliates and operators is clear: the affordability conversation among the player base is not anti-protection, it is anti-clumsy-implementation. There is appetite for safer gambling tools that respect adult autonomy.

"The affordability checks are beyond ludicrous. A small minority of people have an addiction, much like alcohol or drugs, yet the people who are successful at gambling are being punished." - Football, racing & casino bettor, 25–34, £251–£500/wk

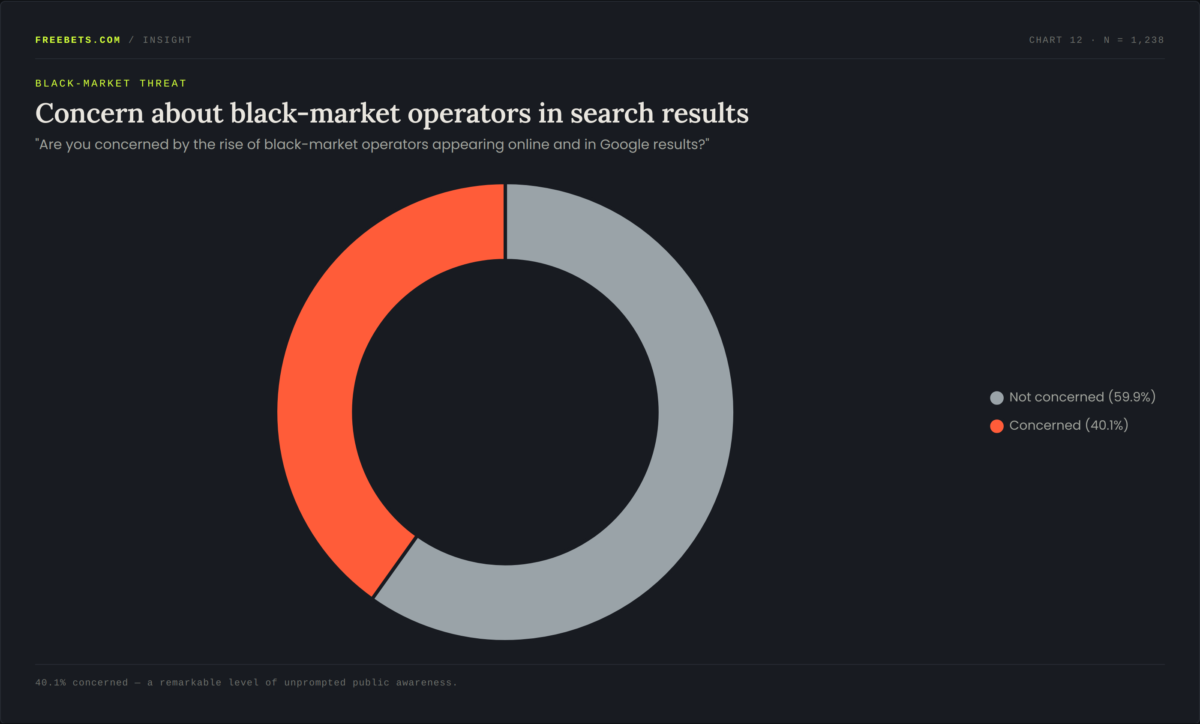

The Black Market Danger: Two in five punters are worried about what they're seeing in Google

This is, in our view, the most consequential finding in the dataset for the licensed UK industry. 40.1% of respondents say they are concerned about the rise of black-market operators appearing online and in search engine results including, explicitly, in Google's organic listings.

This is a remarkable level of unprompted consumer awareness of an issue most often discussed in regulatory and trade circles. It is also a strategic warning: when licensed operators reduce promotions in response to duty pressure, they create a value gap. Unlicensed operators — operating outside RGD, outside affordability obligations, and outside UK tax law, fill that gap with ostensibly more attractive products. Two in five punters are already aware this is happening, and concerned about it.

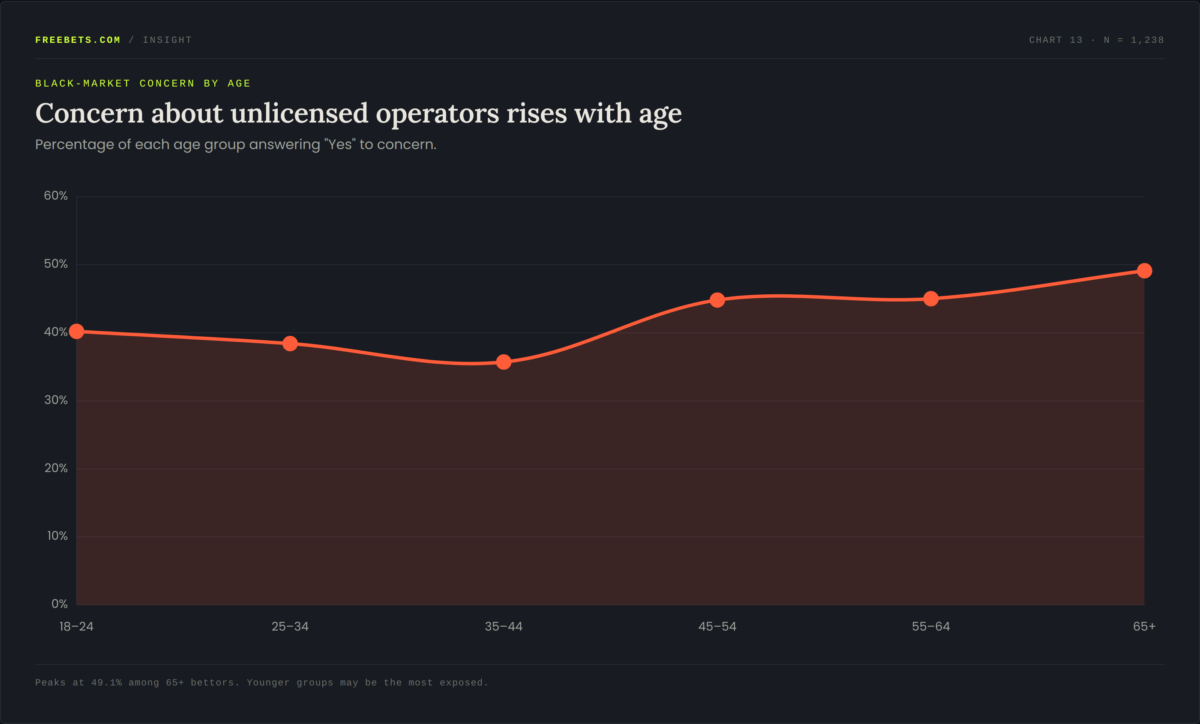

Black-market concern by age

Concern about unlicensed operators rises monotonically with age, peaking at 49.1% among the 65-and-over cohort. The pattern is consistent with older bettors being both more security-conscious online and more likely to engage with traditional media coverage of gambling regulation. Younger bettors, while less concerned, are arguably more exposed: they are the group most likely to engage with influencer-led promotions, social-media-routed traffic, and search-driven onboarding, exactly the channels black-market operators exploit.

"I can totally understand why gamblers would go to black market bookmakers when faced with intrusive checks from licensed operators."

"Black market operators being allowed into Google searches means that legit companies are failing at brand awareness and SEO. " - Football & casino player, 25–34, £0–£100/wk

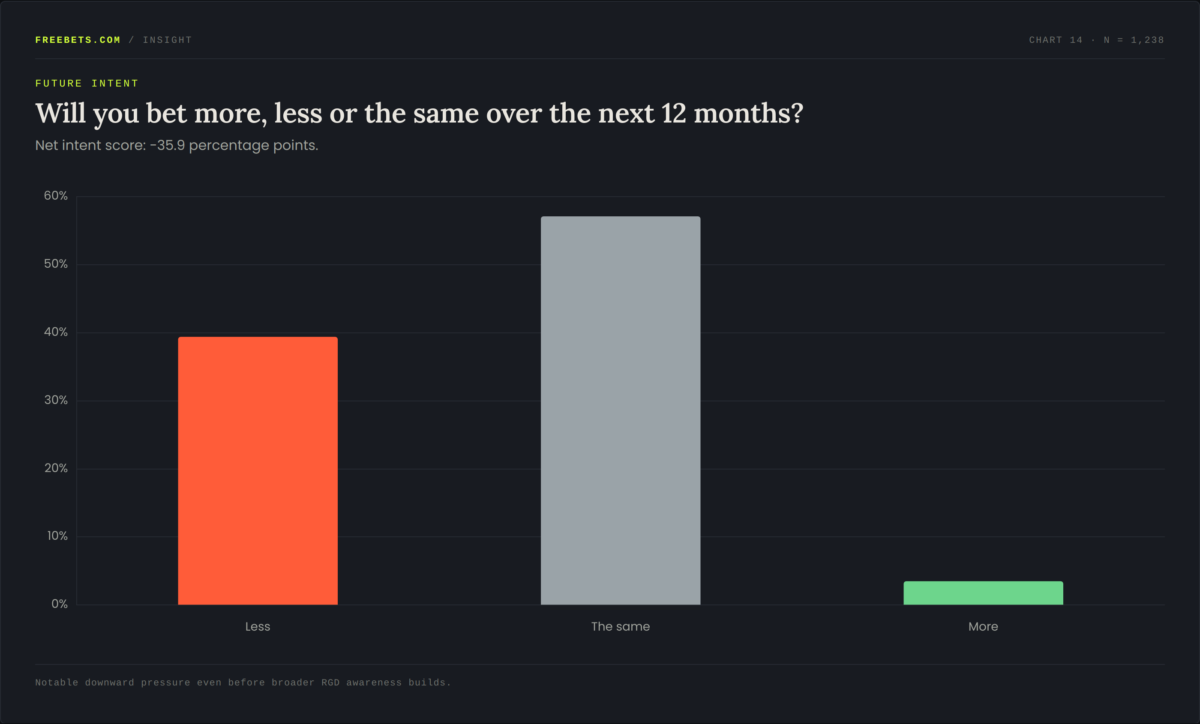

Future Outlook: The market is shrinking, but quietly

The clearest forward-looking signal in the survey concerns intended behaviour over the coming twelve months. The headline number — 57.1% expect to bet "the same", masks a meaningful pull to the downside. 39.4% expect to bet less. Just 3.5% expect to bet more. The net intent score (more minus less) sits at -35.9 percentage points.

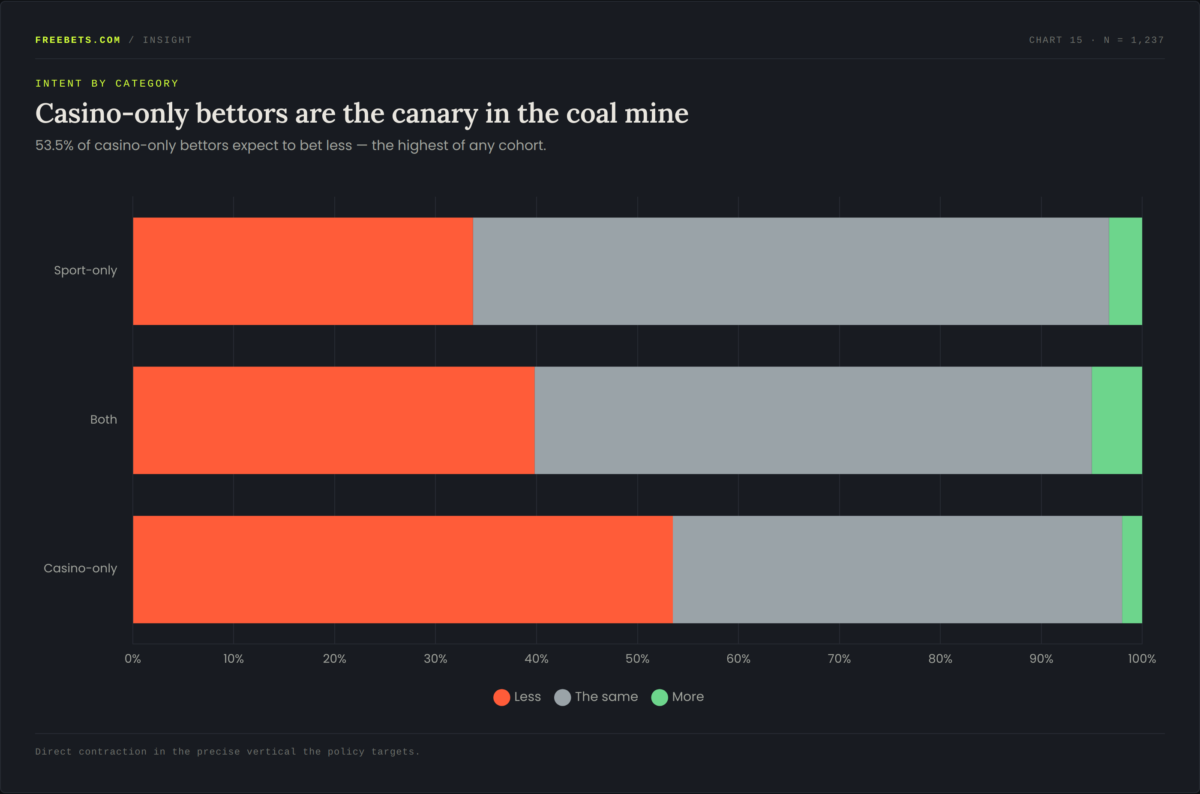

Casino-only bettors are the canary in the coal mine

The single most important behavioural cut in this dataset is intent by player category. 53.5% of casino-only bettors expect to bet less over the next year, comfortably the highest of any cohort, and a full 20 percentage points higher than the sport-only group at 33.7%. Mixed-product (sport-and-casino) bettors sit in the middle at 39.8%.

This is the cleanest evidence in the dataset that the duty hike is producing the behavioural response the industry feared: direct contraction in the precise vertical the policy targets. Casino-only bettors, many of whom may not even know about RGD are, in aggregate, voting with their wallets. For an operator P&L modelling 2026/27 GGR, this should be a sobering data point: the customer base most directly exposed to product degradation is also the cohort most likely to deliver volume loss.

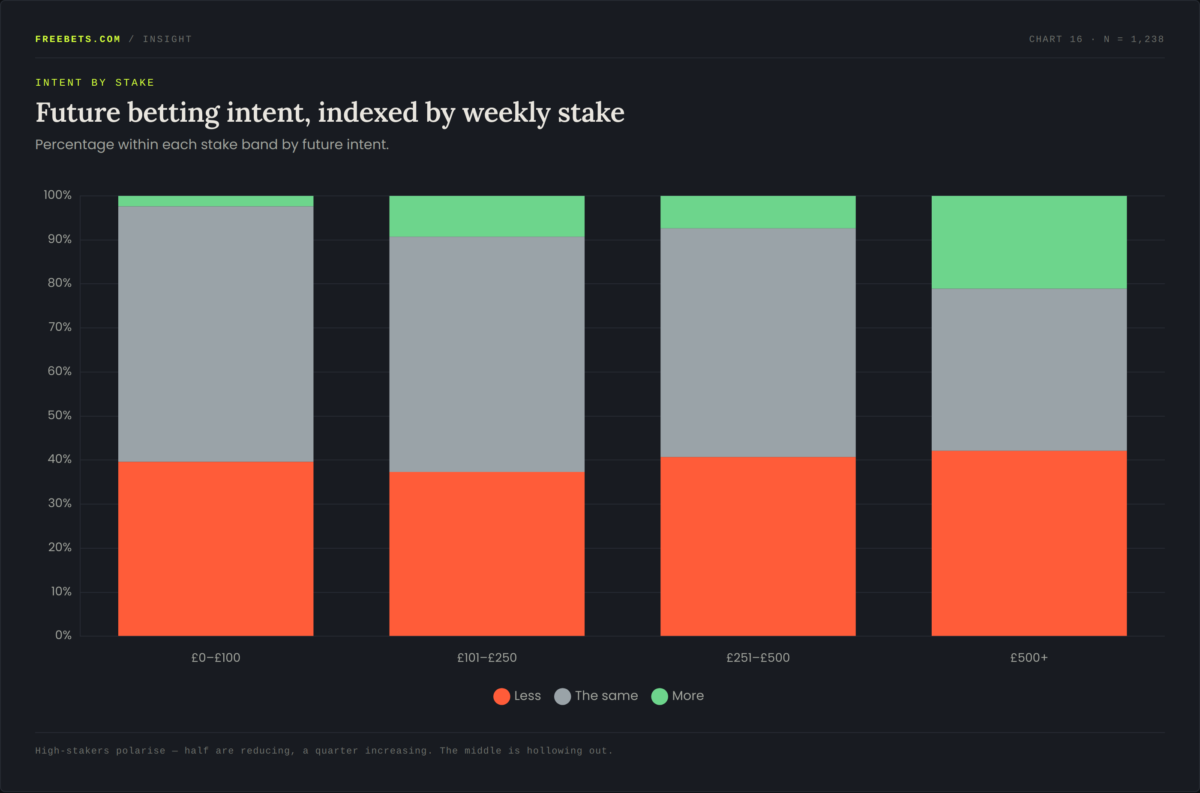

Future intent by stake, the high-stake danger zone

The pattern by stake is similar but with an interesting twist. The downward pull is most pronounced at the top of the staking pyramid: 42.1% of £500+/week punters expect to bet less. But this cohort is also the most polarised, 21.1% of them say they will bet more. These are the customers who deliver the bulk of operator gross gaming revenue, and they are bifurcating sharply.

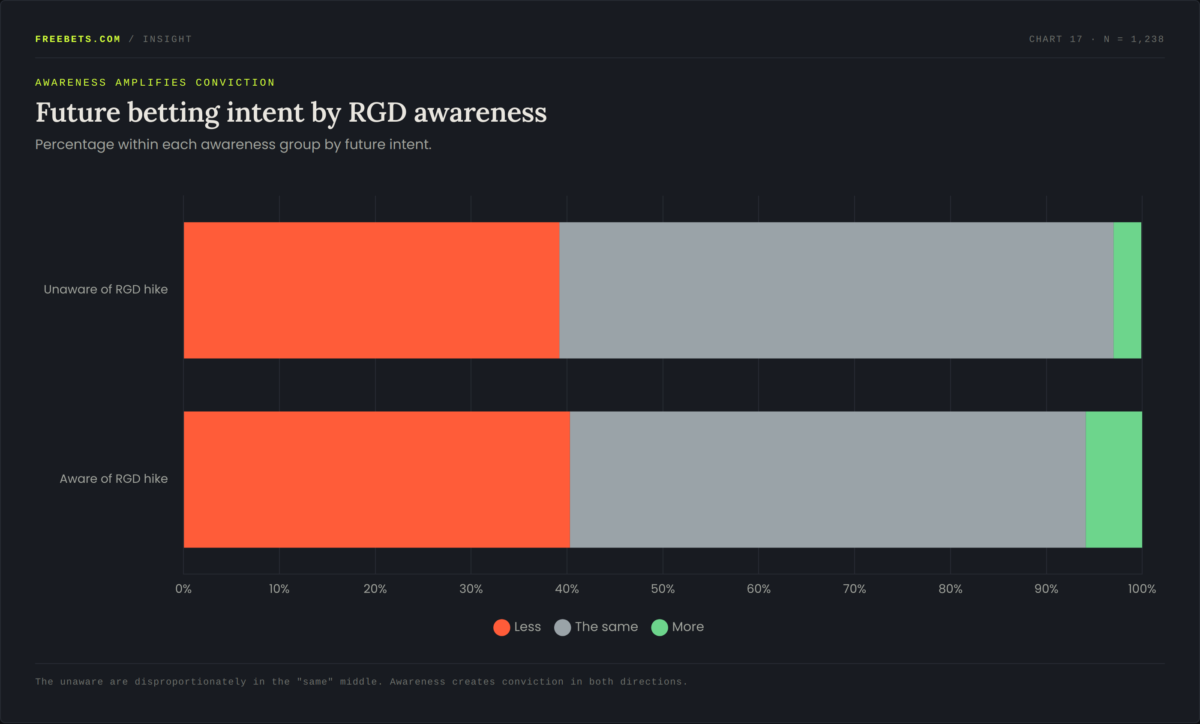

Awareness drives behavioural divergence

One of the more revealing cross-cuts: bettors who are aware of the RGD increase are noticeably more polarised than those who aren't. They are slightly more likely to say they will bet less, but also more than twice as likely to say they will bet more. Awareness creates conviction, in both directions. The unaware sit, for the most part, in the "same" bucket, drifting through the new regime without yet having formed a view.

The implication for forecasting: as awareness inevitably builds, through media coverage, operator communications, or simply through punters noticing further withdrawal of offers, the "the same" middle will collapse. Most of those respondents are likely to migrate to the "less" position rather than the "more" one. The current -35.9pp net intent score should be read as a floor, not a ceiling.

What punters actually want

The free-text "priorities" question delivered the richest qualitative material in the survey. Three themes dominate, in rough order of frequency: better and more frequent bonuses, improved odds and RTP, and fairer treatment for loyal and winning customers — particularly an end to the perceived practice of restricting accounts (colloquially "gubbing") that show profit.

"I would prioritise improving the value offered to players by restoring more competitive odds and meaningful bonuses, while keeping affordability checks streamlined and less intrusive — so they protect users without significantly disrupting the betting experience."— Football & casino player, 18–24, £0–£100/wk

"I feel like offers are just terrible for punters now — there used to be loads of bet-and-gets, now you're lucky to even get money back as free bets."— Football, racing & casino bettor, 18–24, £0–£100/wk

"Forcing betting companies to behave like betting companies and not ban customers who are winning — and abolish taxes on betting proceeds."— Football & racing bettor, 45–54, £0–£100/wk

"Standard odds markets on sports has got worse a little due to demand and supply, thus less chance of finding niche value. Casino play and slot games — I've noticed lesser offers, lesser good offers, and lesser regular payouts in slots."- 20-year veteran bettor, 35–44

A larger and more striking strand of the qualitative responses pushes back hard on the policy direction itself. Punters frame the duty hike as shortsighted, the affordability regime as overreach, and the cumulative effect as a regulated market that is increasingly punishing the responsible majority for the behaviour of a small minority. The language is unusually direct.

"The companies are profitable enough to eat the tax increase — nothing should change. But this is the gambling industry, I'm under no illusions that the customer will eat it."- Football & casino bettor, 35–44, £101–£250/wk

"Government is continuing to overreach and interfere with responsible gamblers and consumers, which is punishing those that stay within their means and they suffer as a result."- Football & racing bettor, 55–64, £0–£100/wk

"Betting is meant to be entertainment, not a way to make money. Offer more bonuses for players to use."- Football, racing & boxing bettor, 18–24, £0–£100/wk

This is the dominant emotional register of the open response qualitative data: punters who view themselves as responsible adults exercising legitimate leisure choices, who feel the regulatory and fiscal apparatus has stopped distinguishing between them and the small minority of at-risk players.

They are explicit about the consequence, that further squeezing of the licensed product is the most reliable way to push consumers toward unlicensed alternatives, exactly as the black-market concern findings suggest is already happening.

"I will probably cease betting altogether in the next 12 months as it is not fun anymore due to constant government and gambling commission interference." - Respondent aged 45–54, £0–£100/wk

Drifting Apart: A Perceived Lack of fairness and fatigue

Across hundreds of qualitative responses, two emotional undercurrents dominate. The first is a sense that the relationship between punter and bookmaker has stopped being reciprocal, that the one-way directionality of risk (bookmakers always win, customers absorb every regulatory and fiscal change) has crossed a tolerance threshold.

The second is fatigue with the experience itself: cluttered apps, payment friction, gummed accounts, and slow withdrawals.

Neither of these is a duty-driven complaint per se. But both are amplified by the duty-driven contraction in offers and odds, which removes the value lubricant that previously masked these structural irritations. RGD being raised to 40% has not created the punter dissatisfaction; it has only increased it further.

Implication and Outlook: What the data tells us about the next twelve months

For UK-licensed operators

The survey paints a picture of a customer base that is unhappy without quite knowing why and that is a more dangerous condition than informed unhappiness.

Operators face a twin challenge: the structural cost of the duty hike, and the brand cost of being seen as the source of degraded value. Without a coherent industry-wide communications effort to attribute the change to its cause, the licensed market risks losing trust at exactly the moment unlicensed operators are visibly closing the value gap.

The 40.1% black-market concern figure should be ringing alarms in commercial, brand and regulatory affairs functions alike. The 53.5% reduction-intent figure among casino-only bettors should be ringing them louder.

For Affiliates

The opportunity here is editorial, not just commercial. With 82.1% of the public unaware of the duty hike and 58.6% reporting a degraded experience, there is enormous demand for plain-English, trusted explainers on what's changed, why offers have shrunk, and how to identify a properly licensed operator.

Affiliates that lean into this educational role, rather than competing solely on offer aggregation will accumulate authority value at a time when authority signals are SEO-critical and regulatory pressure is sharpening. The qualitative responses repeatedly call for "clear odds", "plain English", and "transparency".

The affiliate sector is well-placed to deliver exactly this.

There is also a specific SEO and brand-protection imperative. With 40.1% of punters expressing concern about black-market operators in search results, ranking authoritatively for licensed-only comparison content like our best casino sites guide is both a commercial and a public-interest function.

Affiliate sites' editorial mission for the next twelve months should explicitly include: licensed-operator verification content, RGD-explained content for punters, and Safer Gambling resourcing aligned to the affordability conversation.

For the Regulator and Policymakers

The findings raise legitimate questions about whether the policy intent of the RGD increase is being undermined by its implementation. If the duty was intended to capture revenue from a profitable industry without significantly displacing players towards higher-risk channels, the early evidence is uncomfortable.

Two in five punters are concerned about black-market displacement they can already see in search results.

39.4% expect to bet less in the licensed market over the next year, a portion of whom will not abstain entirely, but will simply migrate.

A serious cross-departmental response, particularly involving HM Treasury, the Gambling Commission, and major online search providers, appears overdue.

For the Punter

For the everyday British bettor, the message from this dataset is to be informed. Understand that the duty change is real, that it is reshaping the offers landscape, and that licensed operators, for all the friction provide consumer protections, dispute resolution, and Safer Gambling tools that black-market alternatives do not. When comparing what's on the table, stick to free bet offers from UK-licensed operators where the safer-gambling tooling, dispute resolution and tax-compliant returns are built in.

The short-term arithmetic of a more generous bonus on an offshore site is rarely the long-term arithmetic of safe, accountable play.

Methodology: How the Data was Collected

The Freebets.com Betting Survey and Trends 2026 Report was fielded online to an audience of 1,238 UK adults who self-identified as active bettors.

Responses were collected throughout April 2026, three weeks after the Remote Gaming Duty (RGD) rate change took effect.

The instrument comprised 13 questions covering demographics, product use, awareness, sentiment and behavioural intent. All free-text responses are reported verbatim with light proofreading.

As with any online self-completion survey, the sample is non-probabilistic. Findings should be read as directional rather than as point estimates of the UK population.

However, the consistency of effects across age, stake and product cuts gives us reasonable confidence that the directional conclusions reported here reflect genuine sentiment in the active-bettor base.

Where stake bands are small (£500+ has n=19), individual percentages should be treated as indicative only; the directional pattern across the four bands remains robust.

Cross-tabs were calculated as row percentages within each cut. Multi-select questions (product mix, perceived ramifications) are reported as percentage of all respondents selecting each option. Free-text responses were thematically clustered but not coded quantitatively.